SEG was launched on 1 January 2020. Each year Ofgem release an annual report. These annual reports give us an insight into the take up of solar in the UK.

By comparing these reports we can see how things have changed over the years since SEG export was introduced. We can also see if any trends have developed.

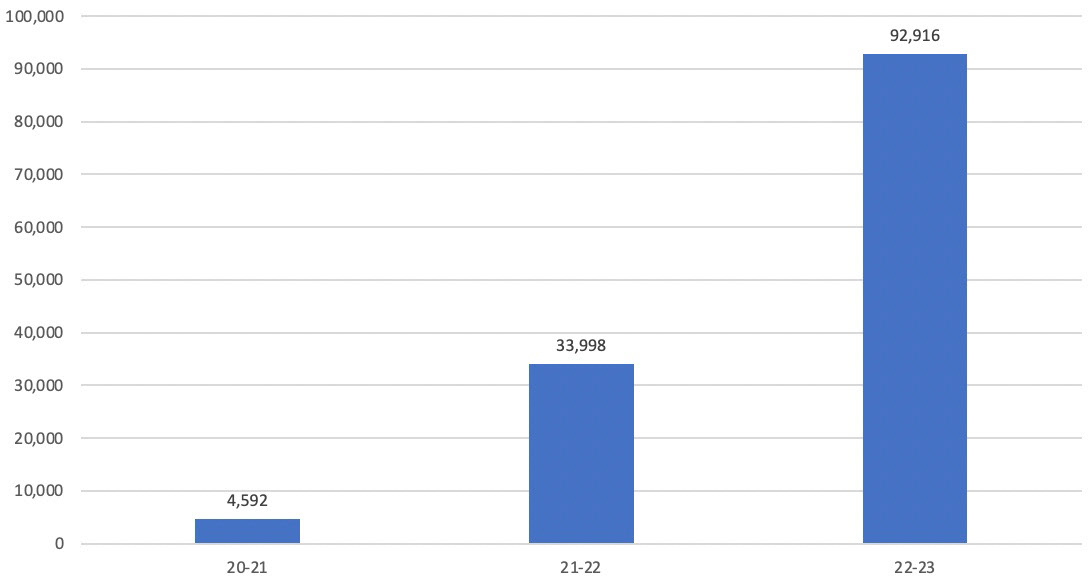

SEG registrations

The first notable trend between the reports are a very noticeable growth in SEG export registrations since the introduction of the SEG scheme.

SEG registrations per year

Each year SEG registrations have increased. The year 2022-2023 has seen the number off registrations nearly triple to 92,916.

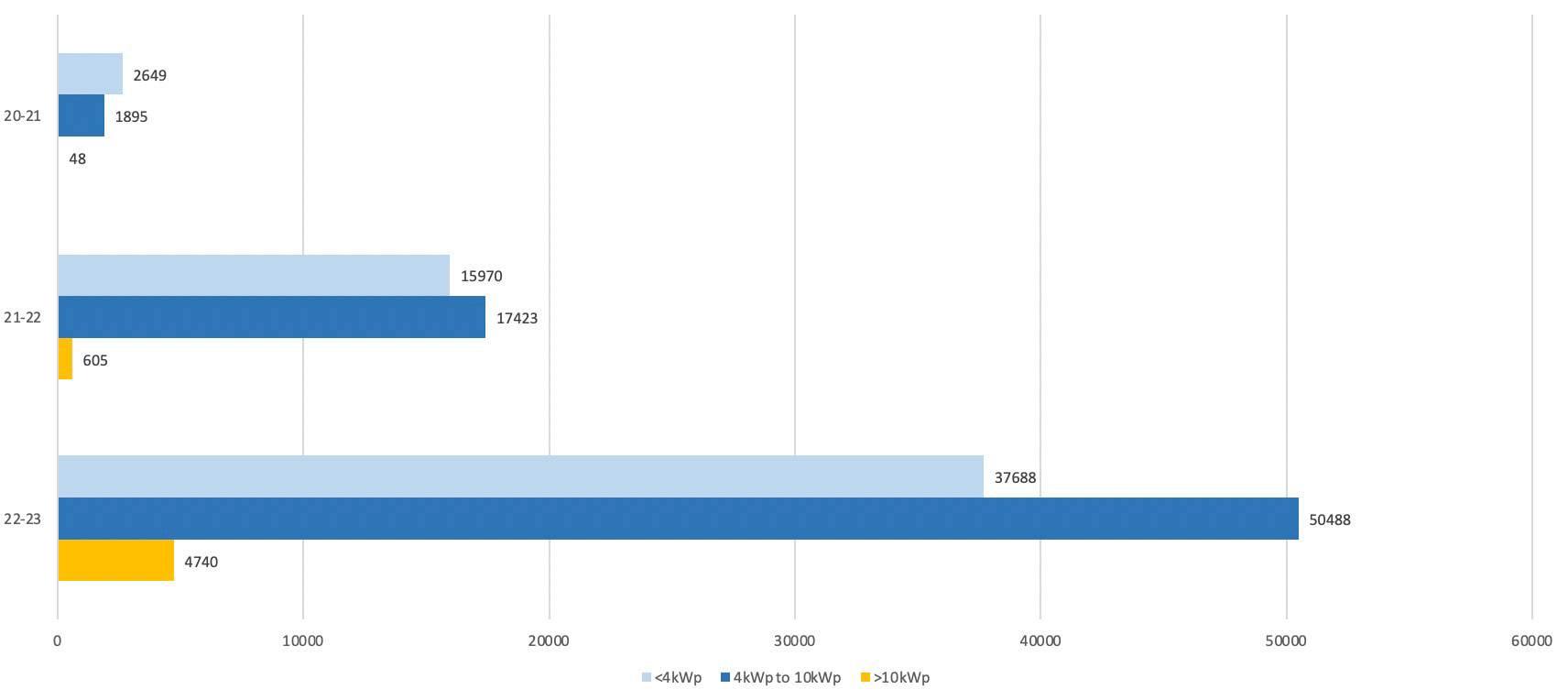

Solar PV installations and capacity

The SEG report not only show the number of solar installations from 2020 to 2023, but also the capacity of those solar installations.

Solar PV installations by capacity range 2020 to 2023

Initially in 2020-21 there were a higher number of solar installations under 4kWp. In the years since the trend has changed towards solar installations with capacity between 4kWp and 10kWp accounting for more than half of all solar installations.

I'd say this is likely down to two reasons, firstly the power output of solar panels has increased to over 400W per solar panel. This means larger capacity systems are now possible from the same footprint compared to using 250W or 300W solar panels.

Another reason could be as solar system prices drop people are looking to maximise the size of their installation to their available space and maximise solar generation. A south facing 5kWp system would likely produce more power than the average household would consume. As we move towards electrification through electric vehicles and heat pumps household electrical consumption will increase. Larger capacity solar systems likely won't be oversized compared to average consumption.

SEG export means you can be paid for excess generation you export to the grid generating an income from the solar installation.

When we look at the capacity size of installed solar in 2022-23 the average installed capacity is 5.3kWp. Solar systems from 4kWp to 10kWp make up 56% of the installed solar capacity with an average size of 5.6kWp. That's 280MWp of solar capacity in this group alone. If we add in solar system below 4kWp that's a combined 289MWp of solar capacity.

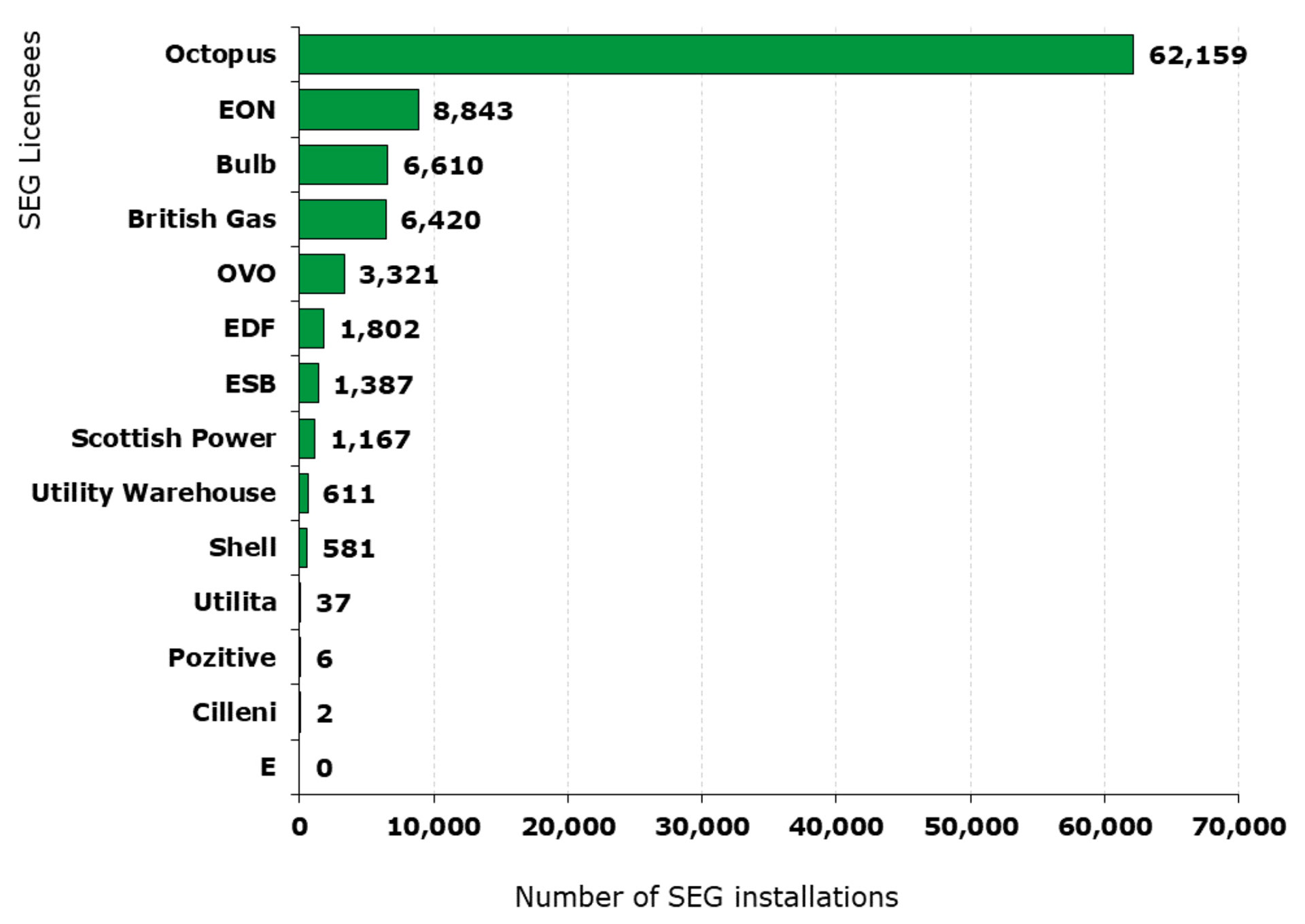

SEG Licensees

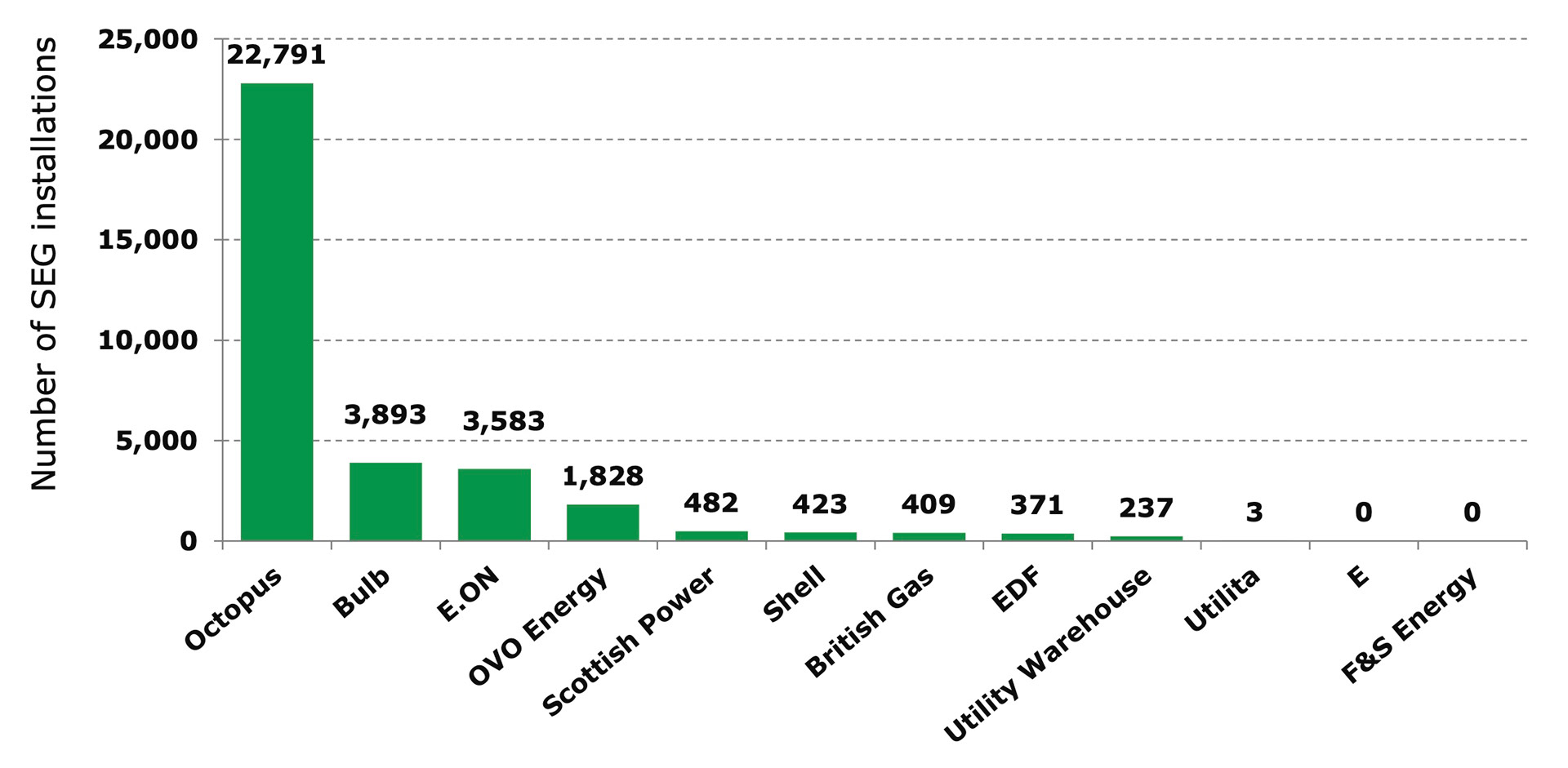

The reports show big changes in SEG licensees since 2020. The most obvious statistic is huge market share that Octopus Energy now have. In 2022-23 62,159 SEG registrations are with Octopus Energy, that's 67% of all SEG registrations. Considering they had just 119 in 2020-21 its a huge increase. Its no surprise when you look at the different SEG tariffs they offer.

When you look at the chart below it's no surprise the energy companies that offer the highest SEG rates have the highest number of SEG registrations. Obviously people vote with their feet by moving to the energy companies that offer the highest SEG rates. I know we did this as we left Utility Warehouse as they offered just 2p/kWh, whilst Octopus offered 15p/kWh.

SEG installations by SEG licensee in 22-23

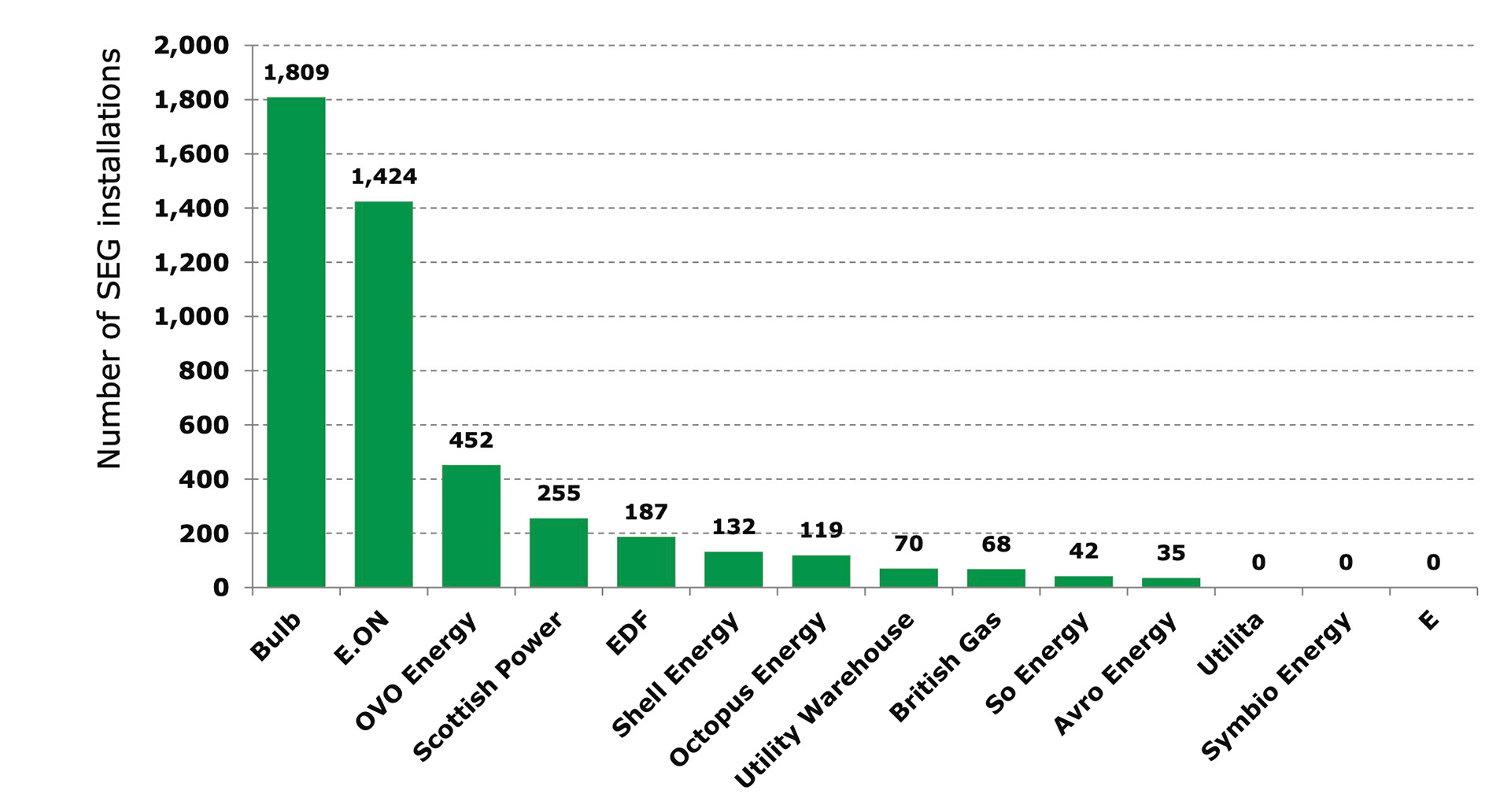

SEG installations by SEG licensee in 20-21

SEG installations by SEG licensee in 21-22

We will likely see some further movement as some energy companies on the 2022-23 chart no longer exist (Bulb). I expect energy companies such as Scottish Power will increase their SEG registrations as they now provide much higher SEG rates of 12p-15p/kWh.

In 2023-24 I expect the top three companies shall likely be Octopus Energy, Scottish Power and British Gas as they offer the highest SEG rates in 2023. We are already seeing evidence of people voting with their feet by moving to Octopus Energy.

Best SEG rates in 2023 - Source: Heatable.co.uk

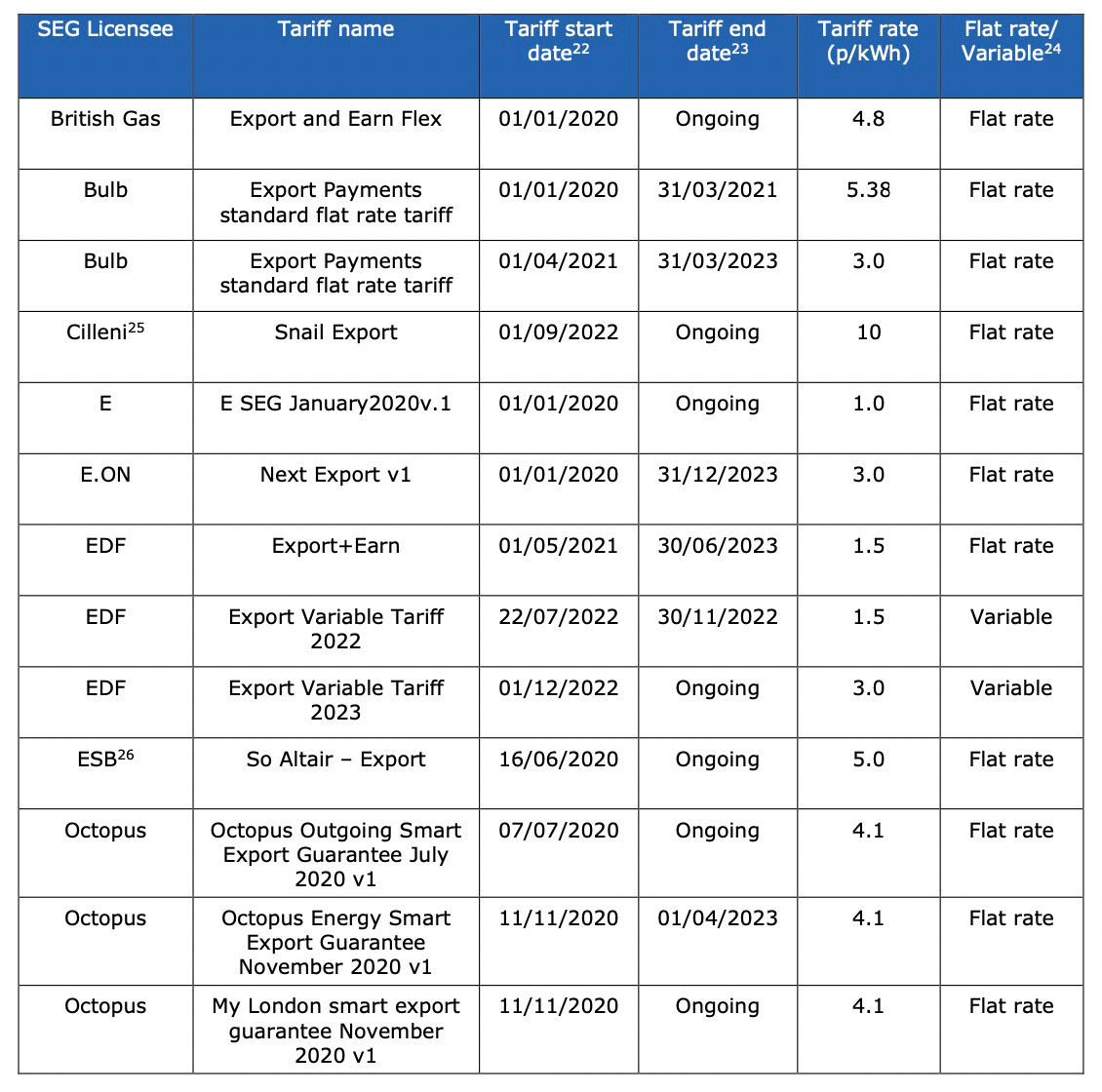

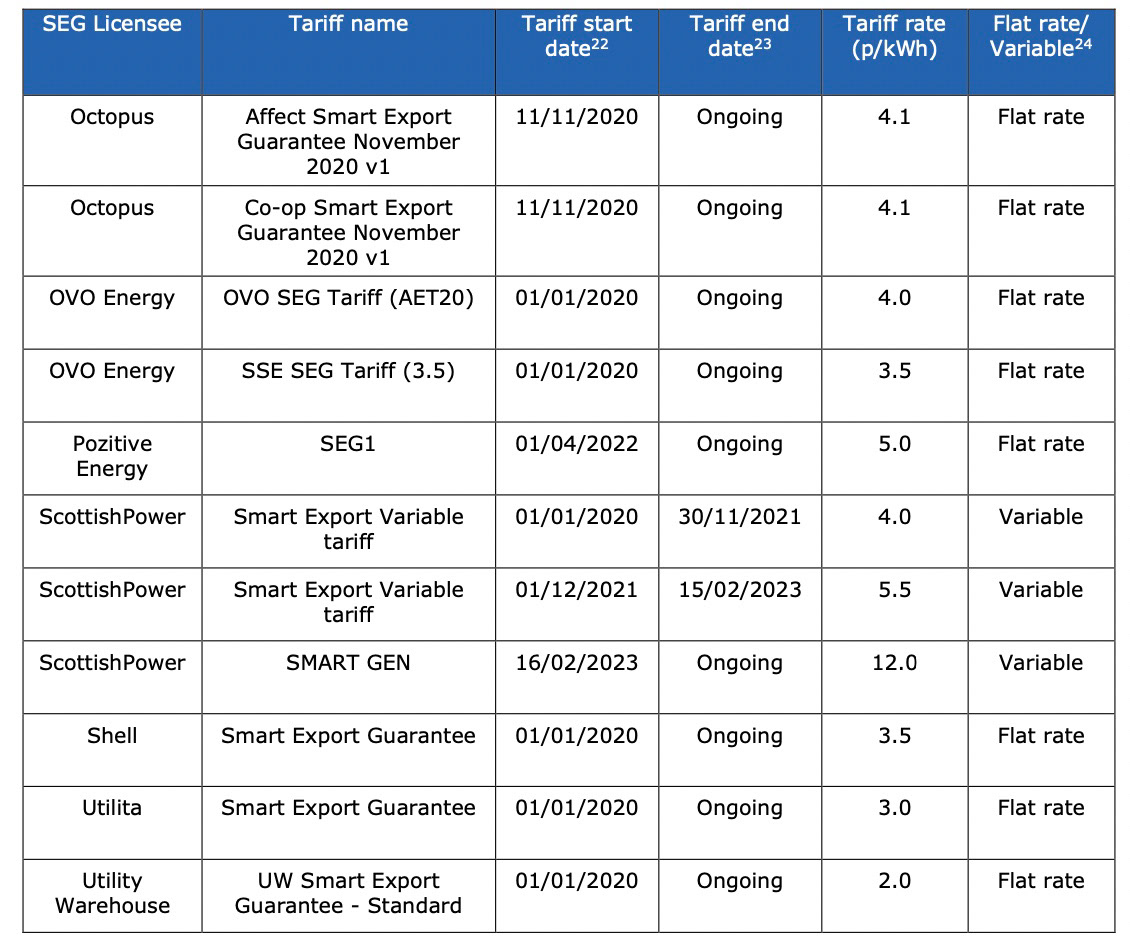

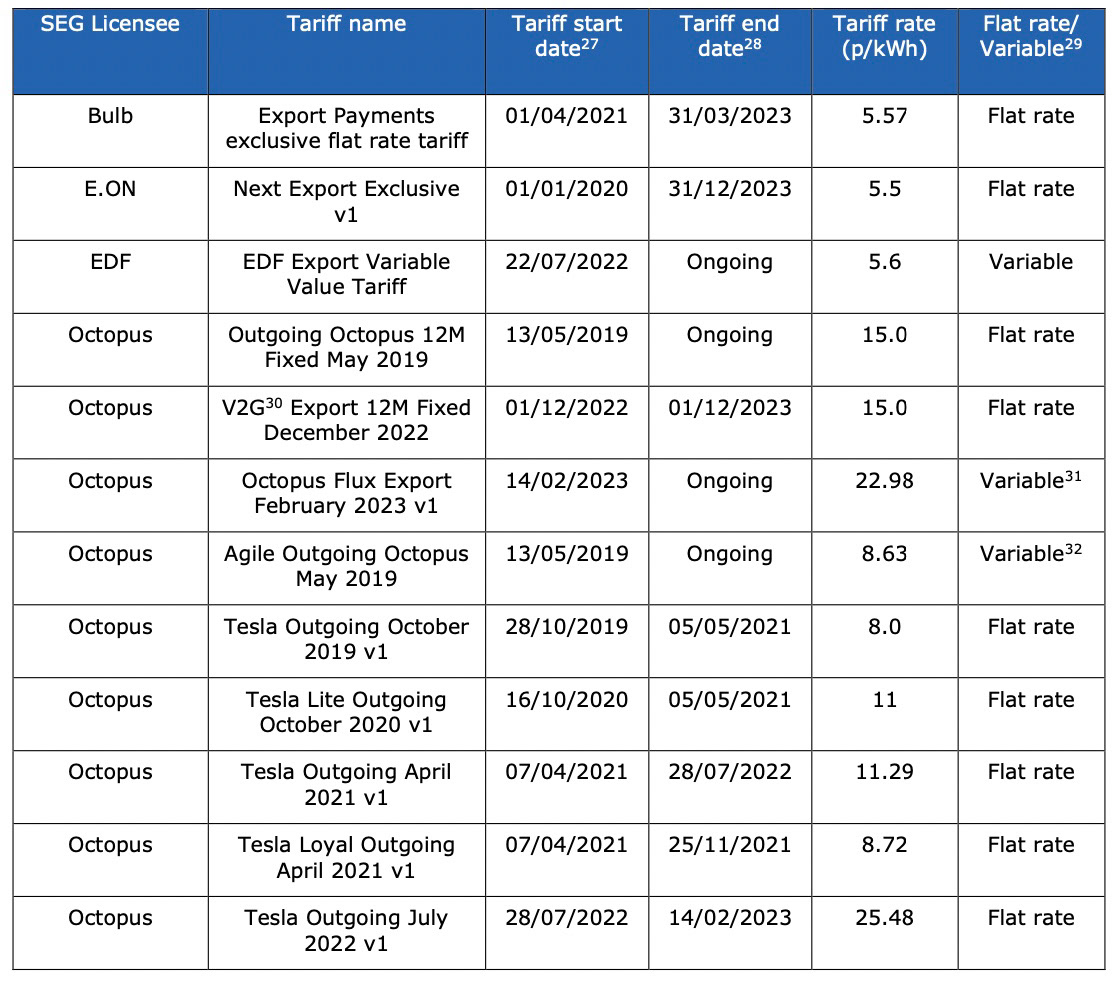

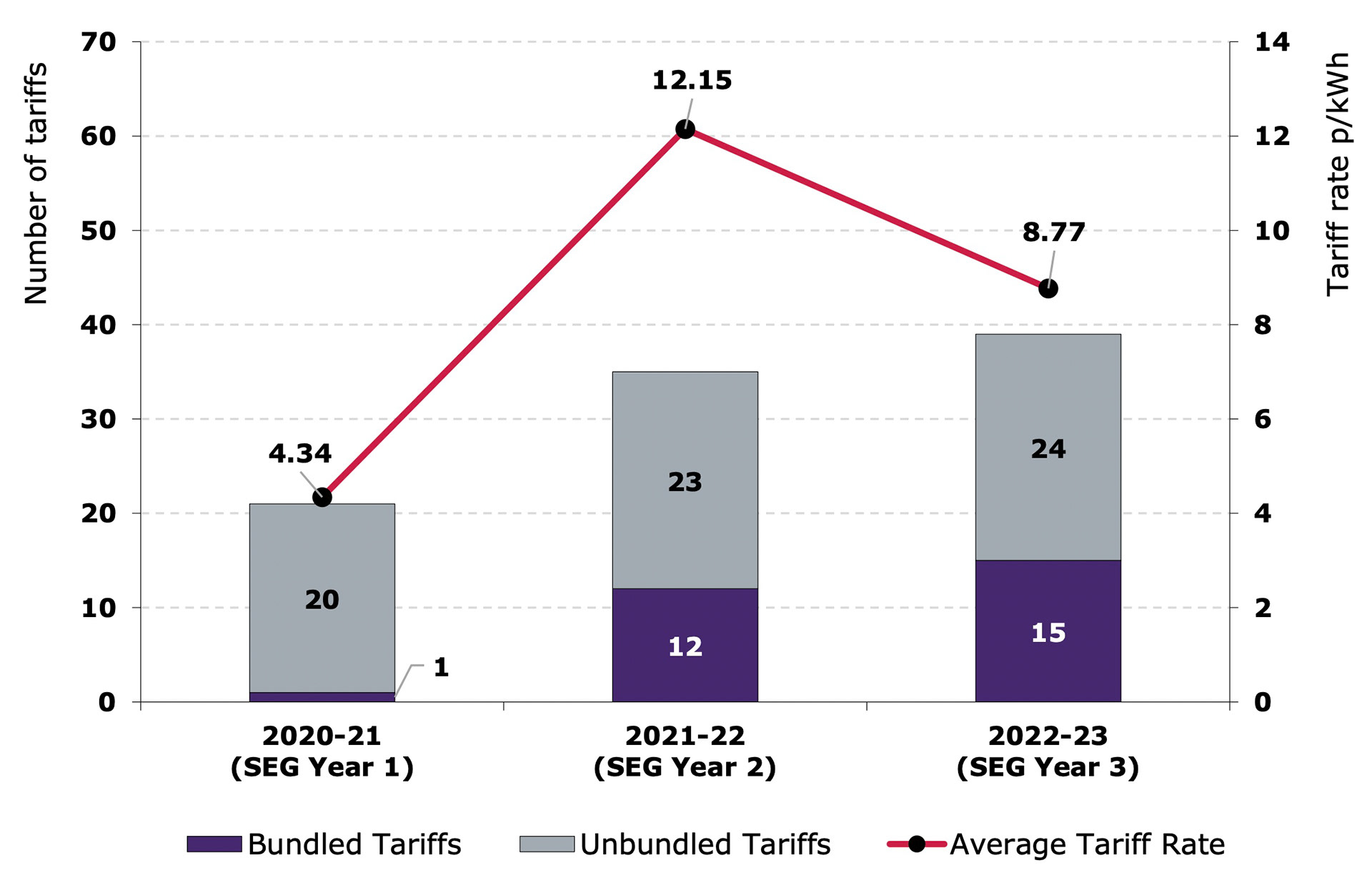

SEG Tariffs

The number of SEG tariffs available has increased year on year since introduction 2020. Whilst the number of unbundled tariffs (each energy supplier with over 150k customer has to provide a SEG tariff) has increased it has been at a lower rate than bundled tariffs.

Unbundled Export Tariffs

Bundled Export Tariffs

When you see the list of unbundled and bundled export tariffs its not surprising to see why Octopus Energy have the highest number of SEG registrations when you see they provide 3 out of 24 unbundled export tariff, and 10 of the 15 bundled export tariffs, and they provide the highest export rate of all energy suppliers.

The graph above showing the average tariff rate is interesting. In 2021-22 it is shown to have averaged 12.15p/kWh. When you calculate the average SEG rate from the total PV payment compared to total PV exported 2021-22 had an actual average SEG rate payout of 6.8p/kWh.The average tariff rates in 2020-21 and 2022-23 are much closer to the actual average SEG rate payouts in those years.

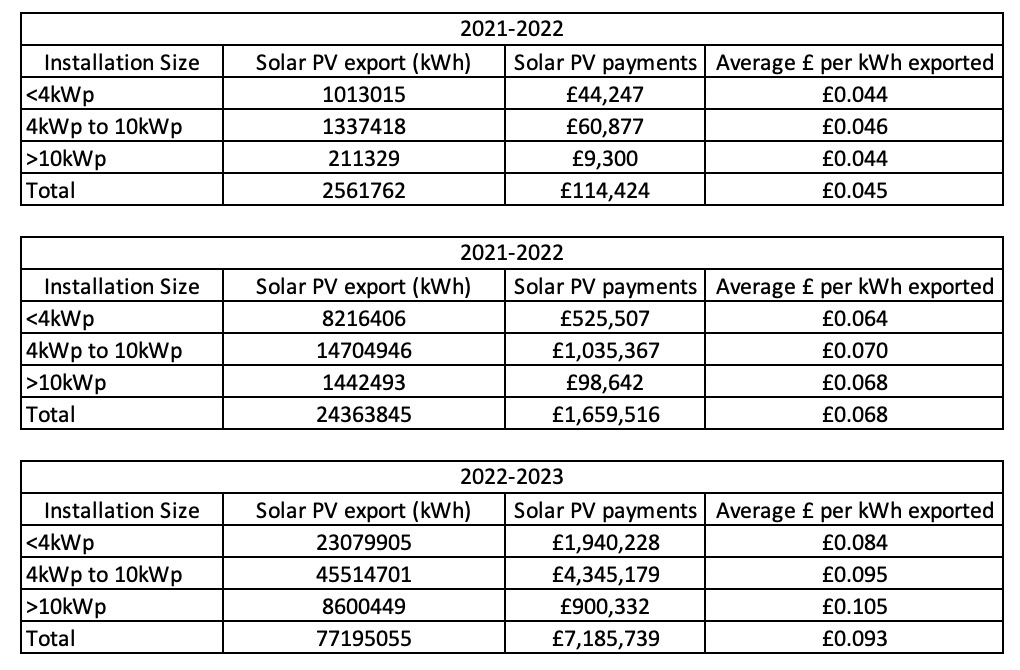

Its clear in the tables actual payment from SEG tariffs have increased year on year from 4.5p/kWh in 2020-21 to 9.3p/kWh in 2022-23.

In 2022-23 the amount of solar exported through SEG tariffs reached 77,195,055kWh, or 77.2 GWh.Thats 3 times the total exported through SEG in 2021-22.

A typical home uses 2,900kWh of electricity per year according to Ofgem. To put 77GWh of solar generation into perspective, that's enough electricity consumed annually by around 26,000 home. 26,000 homes is roughly the size of Macclesfield, Cheshire.

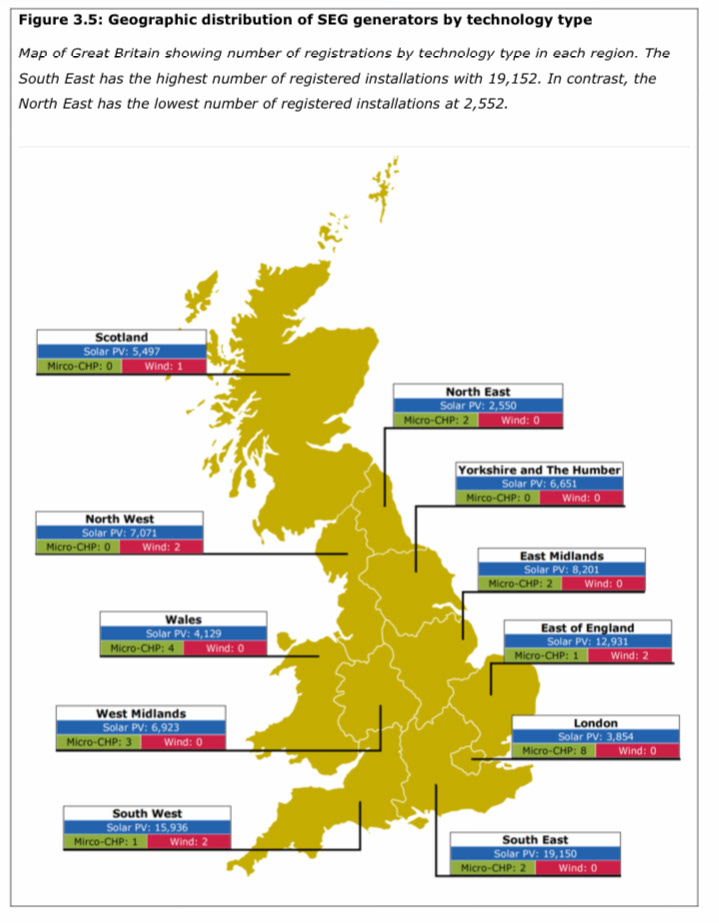

Location of Solar in UK

It's probably not surprising the highest number of solar installations in the UK are in the south where solar generation is generally better. There is still a healthy spread of solar installations in the north of England and Scotland.

The annual SEG reports give a great insight into the changes in solar installations in the UK over the years. I suspect we will see further increases solar in the SEG report as the upward trends continue.